“The future is already here — it’s just not evenly distributed.”

— William Gibson

A quick pulse-check

| Indicator (2023-25) | Latest figure | Source |

|---|---|---|

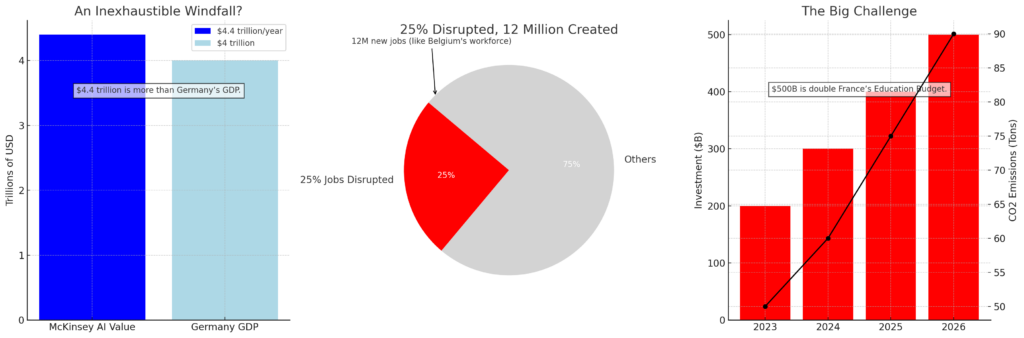

| French jobs fully automatable | ≈ 5 % | Sénat |

| Jobs partly exposed to AI, advanced economies | 40 % | IMF |

| French workers who fear net job losses from AI | 75 % | Labo |

| Finance teams already piloting or running AI | 58 % | Gartner |

| Industrial-robot density, France (2022) | 180 / 10 000 workers | Statista |

| Teachers using AI tools regularly | ≈ 20 % | Le Monde.fr |

The big picture: task take-over, not job wipe-out

France’s own Artificial-Intelligence Commission delivered a sobering — and surprisingly modest — number last spring: only one job in twenty is “directly replaceable” by current AI. The rest will merely be reshuffled, split or augmented. Global-scale anxiety persists, of course: the IMF puts 40 % of jobs in rich economies inside AI’s blast radius, meaning at least one core task could be automated.IMF Yet evidence from INSEE panel data shows AI-adopting French firms hire slightly faster than laggards, because productivity windfalls fund fresh roles in data, compliance and design. (Creative destruction is still creative.)

Sector by sector: who should sweat?

| Sector | Tasks on the chopping block | New (or rising) skills | Current tremor level |

|---|---|---|---|

| Finance & admin | Reconciliations, invoice coding, vanilla risk scoring | Data literacy, model oversight, client storytelling | High – 58 % of teams already run AI; clerical head-counts inch down. Gartner |

| Manufacturing | Repetitive welding, materials handling | Robot maintenance, OT-IT cybersecurity | Medium-high – 6 400 new robots in 2023; density still half Germany’s. IFR International Federation of Robotics |

| Health | Scan annotation, appointment triage | Interpreting AI outputs, patient-side empathy | Low – staff shortages mean augmentation, not cuts. |

| Education | Marking drills, drafting worksheets | Digital pedagogy, prompt-craft | Low-medium – only 20 % of teachers use AI so far. Le Monde.fr |

| Media & creative | Stock copy, basic illustration | Curation, narrative craft, IP savvy | Medium – generative-AI tools flood studios; junior roles feel the squeeze. |

Why the figures matter

- Finance is already living through what McKinsey calls the “augmented-analyst” era: AI now cranks out first-pass pitch books; junior bankers edit rather than build. Clerical attrition is real, but the demand for model auditors and prompt engineers is rising even faster.

- In factories, France’s relatively modest robot density (180 per 10 000) is a cue, not cause for comfort. If Paris wants to “ré-industrialiser” without exporting jobs to cheaper shores, cobots and predictive-maintenance AI are table stakes.

- Hospitals fear burnout more than bots. Radiologists welcome the second pair of silicon eyes; nurses cheer paperwork-eating NLP.

- Classrooms risk a digital divide within the staffroom: unless ministries accelerate the promised AI-literacy charter, the pupils will outrun their profs.

- For journalists and designers, the genie is not going back in the bottle; French unions have already filed clauses limiting uncredited synthetic content.

What the state is doing — and should still do

- Scale training: government pledges to funnel France 2030 cash into nine AI clusters and to push CPF-funded micro-courses in data and model governance. Good — now publish an annual scoreboard of how many clerks, welders and editors actually switched careers.

- Audit the algorithms: the forthcoming EU AI Act will require bias-testing for HR and productivity tools. France could go further and give works councils a veto on opaque “boss-ware”.

- Reward augmentation, not redundancy: offer tax credits for AI deployments that raise per-worker output without shrinking payrolls.

- Target regional safety nets: an algorithmic risk-map (down to département-level) would flag which towns dominated by call-centres or fulfilment hubs need retraining subsidies first.

The bottom line

When the algorithm knocks, most French jobs will not be shown the door; they will be shown a new desk. The threat is less mass unemployment than mass redeployment. Whether that feels like liberation or displacement depends on politics, boardroom choices — and a national willingness to learn faster than the machines.